For the international scholar, securing high-quality health insurance for students in Germany is not merely an administrative checkbox; it is a foundational strategic move. In the Federal Republic, healthcare is a non-negotiable pillar of the Sozialstaat (Social State), reflecting a societal commitment that no resident – regardless of nationality or income – should be left without comprehensive medical protection. Within this framework, health coverage serves as the legal bedrock for your residency and your academic standing.

Key Highlights: Health Insurance for students in Germany

- Why Health Insurance is Mandatory in Germany

- Public vs Private Health Insurance Germany Students

- The True Student Health Insurance Cost Germany

- Best Health Insurance for International Students Germany

- Special Groups: PhD Students and Guest Scientists

- Public vs Private Health Insurance Germany Students: Which to Choose?

- Health Insurance Requirements for German Student Visa

- How to Apply: The Value Package and M10 Process

- Step-by-Step Guide to Securing Your Coverage

- Common Mistakes to Avoid

- Conclusion

- FAQs

Why Health Insurance is Mandatory in Germany

Every resident in Germany is legally obligated to maintain active health insurance coverage. For university students, this obligation is intensely monitored. Your chosen higher education institution does not simply take your word for it; the verification process is entirely digital.

When you apply for a plan, your insurance provider submits a secure electronic notice (historically known as an M10 notification) directly to your university’s administration portal. If this digital confirmation is missing, your student portal will remain locked, and you will be unable to register for classes.

Beyond enrollment, health insurance for students in Germany serves as a core requirement for your legal stay. When you present yourself at the local Foreigners’ Registration Office (Ausländerbehörde) to convert your entry visa into a student residence permit (Aufenthaltstitel), a valid insurance certificate covering the entire duration of your academic stay is among the very first items requested.

Public vs Private Health Insurance Germany Students

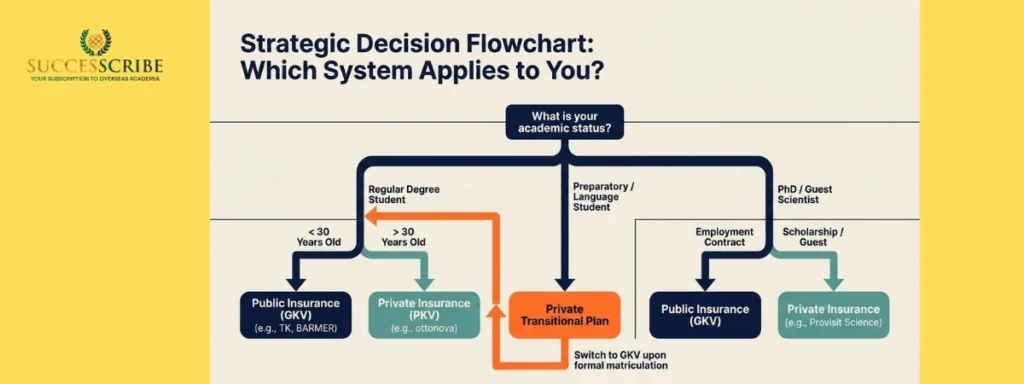

Germany operates on a unique “dual system” composed of Statutory Public Health Insurance (Gesetzliche Krankenversicherung or GKV) and Private Health Insurance (Private Krankenversicherung or PKV). Navigating the landscape of public vs private health insurance germany students requires a clear understanding of your age, academic program, and long-term residency intentions.

To clarify the structural differences, evaluate this comparative breakdown of public vs private health insurance germany students:

| Feature | Public Health Insurance (GKV) | Private Health Insurance (PKV) |

| Eligibility | Primarily degree-seeking students under the age of 30. | Students over 30, language school students, and preparatory (Studienkolleg) students. |

| Contribution Basis | Standardized, government-subsidized student rate linked to the federal BAföG baseline (€855). | Risk-based (calculated according to your entry age, personal health status, and chosen coverage tier). |

| Coverage Scope | Legally defined, standardized benefits across all providers; guaranteed coverage for pre-existing conditions. | Flexible and highly customizable; premium tiers often offer extra perks (like private hospital rooms). |

| Family Benefits | Free co-insurance (Familienversicherung) for non-working spouses and children. | Every family member requires a completely separate contract and individual monthly premium. |

| Doctor Payments | Direct Billing: The clinic scans your health card (eGK) and bills the insurer directly (no out-of-pocket pay). | Upfront Payment: You usually pay the doctor out-of-pocket first and upload the invoice to an app for reimbursement. |

| Estimated Cost | €140 – €155 per month (based on 2026 rates including health base, Zusatzbeitrag, and long-term care). | Varies widely; basic, incoming/preparatory student plans can start around €95 per month. |

Public Insurance (GKV)

- This is the standard choice for most international degree students under 30

- It covers essential services like doctor visits, hospital stays, and basic dental care with no pre-existing condition exclusions

- Popular providers for students include Techniker Krankenkasse (TK) and BARMER.

Private Insurance (PKV)

- Mandatory for those not eligible for public insurance, such as students in preparatory (Studienkolleg) or language courses

- Students over 30 typically switch to private insurance as they are no longer eligible for the discounted public student rate.

- Providers like ottonova and Mawista offer digital-first or tailored plans specifically for international students.

The “No Insurance” Rule: Proof of health insurance is a non-negotiable requirement for obtaining a student visa, completing university enrollment, and registering your residence in Germany

Analytical Prose: The Solidarity Principle vs. Risk-Based Selection

The GKV is built on the “Solidarity Principle.” This means that the healthy support the sick, and those with higher incomes support those with lower incomes. For students, this results in a heavily subsidized, flat-rate premium that is far below the actual cost of care-essentially a gift from the German taxpayer to the international student community.

In contrast, the PKV operates on a “Risk-Based” approach. Private providers, such as ottonova or Provisit, evaluate your individual health profile and age. While this can lead to lower premiums for very young, healthy students in transitional phases (like language schools), it lacks the social safety net of the public system. From a consultant’s perspective, the public system is almost always the superior long-term choice for degree seekers who intend to remain in Germany to work after graduation.

The True Student Health Insurance Cost Germany

A student’s budget is highly sensitive to fixed monthly expenses. Therefore, understanding the exact student health insurance cost germany is essential for realistic financial forecasting.

The student contribution for public health insurance is calculated using a base rate linked directly to the national Federal Training Assistance Act (BAföG) values. As of 2026, the absolute baseline amount used to compute student insurance is fixed at €855.00. Ultimately, choosing the correct health insurance for students in Germany protects both your physical well-being and your legal residency status.

The total monthly public premium is composed of three interconnected parts:

- The Statutory Base Premium: Equal across all public providers.

- The Insurer-Specific Additional Contribution (Zusatzbeitrag): In 2026, the federally targeted average Zusatzbeitrag rose to 2.9%, causing a slight upward push in monthly premiums. Each individual Krankenkasse adjusts this percentage slightly based on its financial reserves.

- The Statutory Long-Term Care Insurance (Pflegeversicherung): Calculated based on your age and whether you have children. For a childless student aged 23 to 29, this component sits firmly at €35.91 per month.

When these components are aggregated, the total student health insurance cost germany for public coverage ranges between €144.00 and €161.00 per month in 2026, depending on your selected provider.

Public Provider Cost Comparison

| Public Health Insurance Company | Monthly Health Base + Zusatzbeitrag | Monthly Care Insurance (Pflegeversicherung) | Total Monthly Student Premium (2026) |

| TUI BKK | €108.76 | €35.91 | €144.67 |

| hkk Krankenkasse | €109.53 | €35.91 | €145.44 |

| Audi BKK | €109.61 | €35.91 | €145.52 |

| Techniker Krankenkasse (TK) | €110.38 | €35.91 | €146.29 |

| HEK – Hanseatische Krankenkasse | €112.09 | €35.91 | €148.00 |

| DAK Gesundheit | €114.74 | €35.91 | €150.65 |

| BARMER | €115.51 | €35.91 | €151.42 |

| VIACTIV Krankenkasse | €123.21 | €35.91 | €159.12 |

By contrast, private student health insurance cost germany options vary far more wildly. Basic, introductory private policies targeted explicitly at international students can begin as low as €35.00 to €79.00 per month.

While these ultra-low-cost private plans appear attractive on paper, they often operate with notable visual deductibles (Selbstbeteiligung), exclude dental procedures, or cap their maximum coverage thresholds for complex hospitalizations.

Premium, full-scale digital private insurance plans for students (such as specialized student tariffs from ottonova) hover around €110.00 to €127.00 per month in 2026, striking a balance between comprehensive private care and a predictable monthly budget.

Best Health Insurance for International Students Germany

Understanding how health insurance for students in Germany works will help you prevent costly delays during your university application phase. Choosing the right provider is a strategic decision based on your specific academic path.

| Provider | Type | Target Group | Key Advantage |

| TK (Techniker) | Public | Degree Students < 30 | Top-rated English App & TK-Flex Bonus. |

| BARMER | Public | Degree Students < 30 | Multi-state network & English Hotline. |

| ottonova | Private | Students > 30 / Prep | Elite Digital concierge; fast refunds. |

| Mawista/Provisit | Private | Language/Transitional | Low-cost entry; Embassy-approved. |

Analytical Prose: Justifying the Leaders

TK is consistently ranked as the best health insurance for international students germany offers due to its seamless digital interface and proactive English-language support. However, for a student over 30, paying €275 for “voluntary” public insurance is often economically inefficient. In such cases, ottonova’s private student tariffs (around €144) provide better specialized benefits – such as enhanced dental and vision coverage – at a significantly lower price point.

Special Groups: PhD Students and Guest Scientists

A “Complete Guide” must address those outside the standard undergraduate mold.

- PhD Students: If you have an employment contract with the university (e.g., as a research assistant), you are automatically eligible for the public system, with contributions split between you and the university. However, if you are a scholarship holder, you are considered “self-funded” and generally must take private insurance if you are over 30.

- Guest Scientists: Researchers visiting for short periods (less than one semester) may be able to use their home country’s insurance if a social security agreement exists. However, for visa purposes, a specialized “Guest Scientist” plan (like Provisit Science) is recommended to ensure the embassy accepts the coverage without delay.

Preparatory Courses and Language Schools

If your entry visa requires you to complete a preparatory foundation year (Studienkolleg) or a sequence of intensive German language courses prior to stepping onto your official degree path, you are not eligible for public student insurance. The public system classifies you as a non-regular student during this interim phase. You must utilize a private transitional plan. The moment you clear your entry exams and formally matriculate as a full-time, regular university student, you gain the immediate right to drop your private plan and enroll in a standard public Krankenkasse.

Public vs Private Health Insurance Germany Students: Which to Choose?

This decision has long-term residency implications that most students overlook.

| Feature | GKV (Public) | PKV (Private) |

| Switching Back | Always possible to go private. | Permanent Lock-in; cannot return. |

| Working Student | Automatic coverage if < 20 hrs. | May require premium adjustments. |

| Career Entry | Seamless transition to work. | Must re-evaluate eligibility at job start. |

| Payment | Cashless (Card only). | Pay upfront; 2-4 week reimbursement. |

The “So What?” Layer: The Permanent Lock-In Effect

When debating public vs private health insurance germany students must understand the “opt-out” rule. If you are eligible for public insurance but choose to take a private policy for your degree, you must sign an “Exemption from Mandatory Insurance.” This decision is permanent for the duration of your studies. You cannot switch back to the public system just because you decide you want family coverage later. For students who plan to make Germany their home, staying in the GKV is the most strategically sound path.

Health Insurance Requirements for German Student Visa

Your university enrollment remains completely blocked until a valid policy for health insurance for students in Germany triggers the digital notification to the campus portal. The German Embassy requires specific, verifiable documentation to approve your visa application.

Visa-Compliant Insurance Checklist

| Document Name | Issuer | Purpose |

| Versicherungsbescheinigung | GKV or PKV Provider | Proves long-term coverage for the university. |

| Incoming Insurance | e.g., Provisit Visum | Bridges the gap from landing to semester start. |

| M10 Notification | Public Insurer | Digital confirmation sent directly to university. |

Analytical Prose: The EU/EHIC Gap and “Incoming” Needs

Students from the EU often assume their EHIC (European Health Insurance Card) is sufficient. While true for medical care, you cannot enroll without a German public insurer issuing a “Confirmation of Exemption.” Furthermore, degree students from non-EU countries often arrive in September but their policy only starts October 1st. You must have “Incoming Insurance” for those transitional weeks; otherwise, your visa will be rejected. Providers like Expatrio and Fintiba bundle this “Incoming” coverage for free within their Value Packages.

How to Apply: The Value Package and M10 Process

The modern application process is dominated by “Value Packages” from platforms like Expatrio or Fintiba.

- Selection: You apply for a Blocked Account and health insurance simultaneously.

- The M10 Digital Trigger: Once you upload your admission letter, the insurer (TK or BARMER) triggers an M10 Notification to your university.

- Activation: Upon arrival, you upload your German address and visa to activate your health card.

The “So What?” Layer: The Danger of Manual Submissions

I strongly advise against trying to handle the insurance notification manually. If you simply email a PDF to the university, it may sit in an inbox for weeks. The M10 digital notification is a server-to-server handshake between the insurer and the university. Without this digital trigger, the university’s system will flag you as “uninsured,” potentially blocking your ability to register for classes or exams.

Step-by-Step Guide to Securing Your Coverage

To ensure zero friction during your relocation, follow this precise, chronologically structured operational checklist to get your health insurance for students in Germany active and verified.

| Step | Phase / Timeline | Core Action Required | Goal / Outcome |

| 1 | 1 – 2 Months Before Departure | Choose your insurance provider (e.g., Public like TK/BARMER for degree students, or Private for language students). | Select a plan that matches your age and course type. |

| 2 | Before Applying for Visa | Submit your application online via the provider or a blocked account bundle portal. | Initiate your registration using your passport and university admission letter. |

| 3 | Within 24 – 48 Hours | Receive and download your digital health insurance certificate. | Use this official document to satisfy your mandatory German student visa application. |

| 4 | Upon Arrival in Germany | Your insurance provider sends an automated digital notice directly to your university. | Clear the campus health insurance check to finalize your official enrollment. |

| 5 | First 2 Weeks in Germany | Provide your local German bank account details (IBAN) to your insurance company. | Set up an automated monthly direct debit for your premium payments. |

| 6 | First Month of Classes | Upload a passport-style photo to your insurer’s smartphone app. | Receive your physical electronic health card (eGK) delivered directly to your mailbox. |

Common Mistakes to Avoid

In my years of liaison work, these three errors cause 90% of student insurance crises:

- Relying on “Travel Insurance”: Standard travel insurance from companies in India, China, or the US is almost never accepted for university enrollment. It lacks the “substitutive” depth required by German law.

- Missing the 3-Month Window: If you want to use private insurance, you must apply for your exemption from the public system within the first 90 days. If you miss this, you are legally locked into GKV.

- Ignoring the Nursing Care Component: When calculating the student health insurance cost germany requires, always ensure your quote includes Pflegeversicherung. Some “cheap” online quotes omit this, leading to a rejected visa application because the coverage is legally incomplete.

Conclusion

The decision between public vs private health insurance germany students must make is the first major hurdle of your international education. For most degree-seekers under 30, the public system – specifically through Techniker Krankenkasse (TK) or BARMER – offers the most secure and frictionless experience. For those in transitional language courses or those over 30, private providers like ottonova and Provisit offer the legal compliance necessary to secure your visa.

The “best” insurance is the one that aligns with your age, your course duration, and your long-term career goals in Europe. By accurately budgeting for the 2026 student health insurance cost germany requires – approximately €141 to €155 for public coverage – you protect your academic investment. This guide remains your definitive 2026 resource for mastering health insurance for students in Germany and ensuring your focus remains on your studies, not your paperwork.

FAQs

Question. Is health insurance really mandatory?

Answer. Yes. Under German law, every resident must be insured. It is a prerequisite for your visa and your university enrollment.

Question. Can I use insurance from my home country?

Answer. Only if you are from the EU (EHIC) or a country with a social security agreement. Even then, you must get a German insurer to certify your exemption for the university.

Question. What exactly is the M10 notification?

Answer. It is a digital report sent by your German insurance company to the university database confirming you have valid coverage. Enrollment is impossible without it.

Question. Does the insurance cover dental and vision?

Answer. Public insurance covers basic dental (fillings, check-ups). Private plans like ottonova often offer superior vision and dental benefits as part of their standard student package.

Question. Can I switch from private to public during my studies?

Answer. Almost never. Once you opt out of the public system to go private, you are “locked in” until you graduate and start a full-time job.

Related Post

Student accommodation options in Germany

Cost of living in Germany city wise comparison

German spouse visa for Indian students

Germany blue card for Indian professionals